Making Markets Work: A Participatory Study of Specialty Coffee and Domestic Value Chains for Farmers| 25, Issue 25

An interdisciplinary research team from Switzerland, Bolivia, and Colombia, led by CHAHAN YERETZIAN, NELSON GUTIÉRREZ GUZMÁN, JOHANNA JACOBI, and including researchers Derly Lara, Daniel Castro, Sebastian Opitz, Sabine De Castelberg, Sergio Urioste, and Alvaro Irazoque, worked alongside coffee farmers, processors, and traders to examine which value chain structures improve farmer livelihoods in the Yungas of Bolivia and Huila, Colombia.

Photo Credits: Chahan Yeretzian, Nelson Gutiérrez Guzmán, Johanna Jacobi, Derly Lara, Daniel Castro, Sebastian Opitz, Sabine De Castelberg, Sergio Urioste, and Alvaro Irazoque

Introduction by KIM ELENA IONESCU, SCA Chief Strategy Officer

At an SCA conference in 2018, Professor Chahan Yeretzian from the Zurich University of Applied Sciences (ZHAW) shared with me that he was starting to work on a research project related to coffee farmer livelihoods in Colombia and Bolivia. He wanted me to be aware of the project, he told me excitedly, because he was looking forward to sharing the findings with SCA members when it concluded. I found myself wondering how he could possibly be thinking so far ahead—research takes years, after all! —but his enthusiasm was infectious, so as soon as their research was published in the journal World Development Perspectives in 2024, I eagerly dug into it.

The first thing that struck me was how ambitious the scope of the research is: Colombia and Bolivia are big countries with diverse coffee production systems, so the research team from Zurich University of Applied Sciences (ZHAW) had to make strategic choices about which similarities and differences to focus on as they sought to understand how farmers use specialty coffee to increase their income. Colombia exports a lot more coffee than Bolivia and its domestic market is larger, but Bolivia’s unusual value chain for dried coffee skins (sultanas) will be a source of inspiration for anyone interested in exploring creative opportunities for value addition.

As I read further, I thought about the rapid growth in domestic consumption of specialty coffee in coffee-producing countries around the world since the research began. While most of the high-value coffees produced in Bolivia and Colombia are exported, domestic markets increasingly offer alternatives. Selling to a local roaster will not be the most profitable option for every farmer, everywhere (and for some farmers it will not be an option at all), but this research emphasizes the importance of understanding all possible options because (to paraphrase the authors) value chain structures have a greater impact than cupping scores on how much a farmer earns.

In addition to presenting insights about coffee farmer incomes in Colombia and Bolivia, this study also reminds curious readers that it’s not only what question we ask, but how we ask them, that matters. The team chose to use a participatory action method for their research that prioritizes inclusion and avoids generalizing the experiences of individuals, whether they are from different countries or from the same community. By taking time to understand and document the needs, challenges, and strategies of coffee producers in Bolivia and Colombia, these researchers have created a record that contributes to the industry’s collective knowledge and potential for creativity in coffee value chains worldwide.

- KIM ELENA IONESCU, SCA Chief Strategy Officer

Clockwise from bottom right: Harvested coffee fruits, fruit exocarp (outer skin), pulped coffee , dried fruit exocarp. Image credit: Azafrán Bolivia.

The specialty coffee sector has spent years trying to improve farmer livelihoods by focusing on coffee prices. But prices are connected to how, where, and by whom coffee is processed and how it is sold through value chains.

In Colombia and Bolivia, specialty coffee has traditionally been exported. But domestic markets are now growing, creating new opportunities for farmers to sell coffee and coffee-cherry products closer to home. We wanted to understand different value chains and how they impact farmers’ livelihoods.

We launched a research project designed to understand how value chains function from the perspective of those who work within them.[1] Our study was conducted during a period of particularly low coffee prices (2017–2020, overlapping with a period sometimes known as a coffee price crisis) and used a participatory methodology that allowed us to work collaboratively with farmers, processors, traders, and other stakeholders.

We investigated the market and livelihood potential of specialty coffee value chains on smallholder farmers in the Huila Department of Colombia and the Yungas region of La Paz in Bolivia. We chose Colombia as an example of a specialty coffee sector with relatively established domestic consumption[2] and established export markets. Bolivia represented a more emerging context, with a tradition of consuming coffee-cherry products (cascara, known locally as sultana) and a relatively new specialty coffee production and consumption market. Our research questions included:[3]

How are different specialty coffee and coffee-cherry value chains in Bolivia and Colombia organized in terms of actors, relationships, and profits?

What impact do different value chains have on smallholder farmer livelihoods?

Our research revealed different pathways toward profitability in each context. There were substantial profitability gaps between different value chain types—including a nearly ninefold difference in returns between the most and least profitable value chains in Colombia. These differences weren’t primarily driven by coffee quality or farming efficiency, but by structural factors, such as who controls the processing and who has direct market access. We also investigated the challenges and trade-offs associated with different value chain types.

Product development workshop in Huila with different stakeholders from the coffee sector.

Participatory Action Research: Value Chain Actors as Researchers

Our research approach was grounded in a “participatory action research.” This meant that we wanted to draw on the lived experience of participants, with the aim of not only understanding their perspectives, but also doing something together. The research brought together four public universities (two in Switzerland, and one each in Bolivia and Colombia), one small local coffee company in each context, and Slow Food in Bolivia.

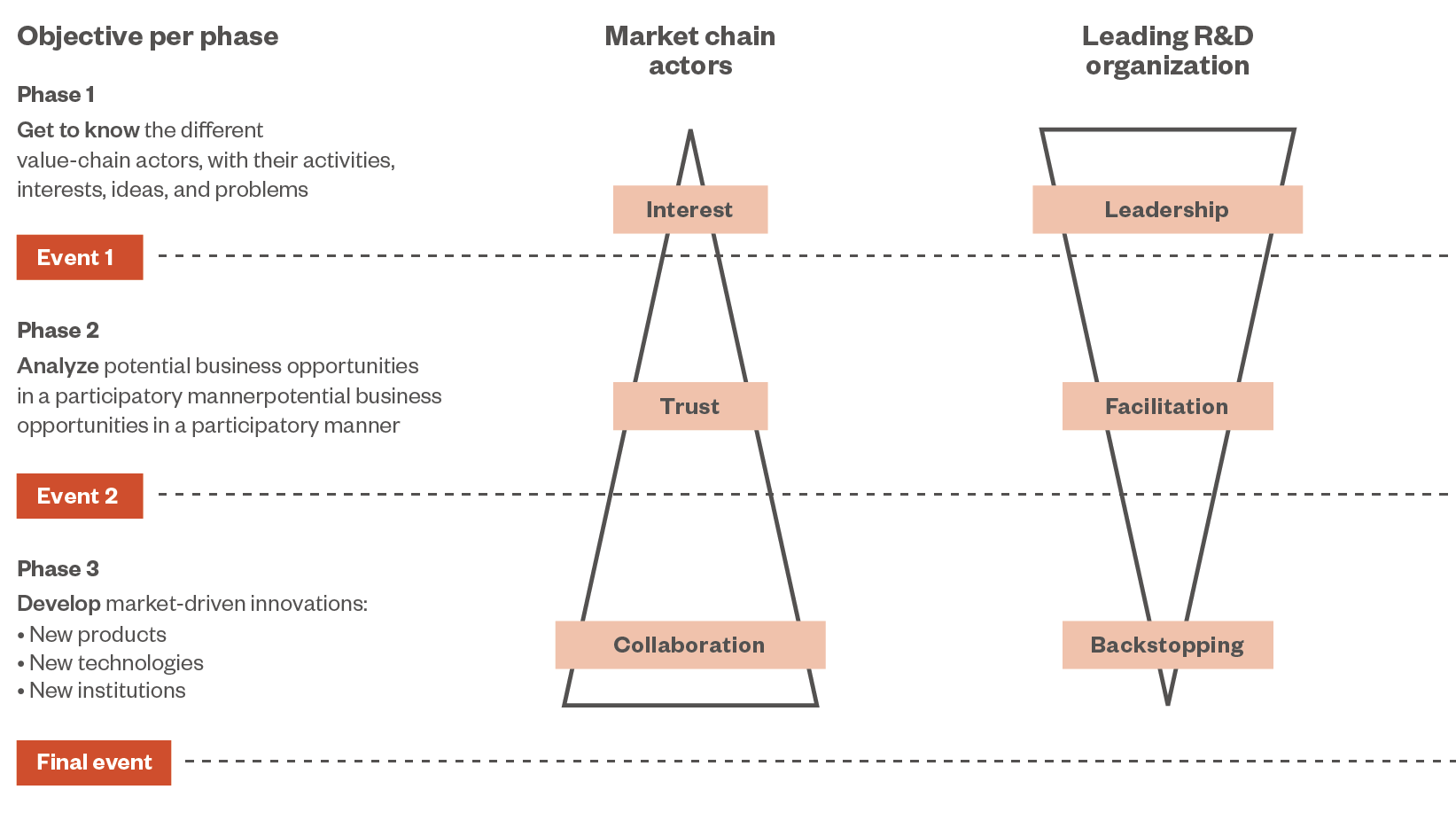

We used part of the “participatory market chain approach” (PMCA)[1]—an approach developed in Peru that involves actors developing innovative products and value chains together, with a focus on sustainable rural development. One of the key features is the collaboration between diverse stakeholders. Our research team had a role as facilitators—a role that decreased over time as stakeholders assumed more and more ownership over the process (see figure 1).

Figure 1. In our study, the researchers led at first, while the practitioners’ interest was still low. The researchers built trust and facilitated exchange and the development of ideas and networks, and later the researchers provided a support-only (backstopping) role while the market chain actors led and collaborated among each other. This figure is adapted from Jacobi et al., 2024.

In practice, this meant organizing participatory workshops in both countries where farmers, processors, local traders, exporters, and buyers came together to collectively map their value chains. The workshops also focused on specialty coffee marketing strategies and strengthening small coffee businesses for local markets in Colombia and on specialty coffee-cherry (cascara or sultana) products in Bolivia. We conducted two workshops with multiple stakeholders in each context: one at the start and one at the end of the two-year project.

Between the workshops, we also conducted semi-structured interviews with 43 actors in Colombia and 73 actors in Bolivia (including farmers, cooperatives, intermediaries, roasters, exporters, and traders), as well as online consumer surveys about coffee preferences, and spent extended time with eight farming families in Colombia and four in Bolivia. Using these sources and wider research, we conducted a cost–benefit analysis for selling both specialty coffee[2] and commodity coffee,[3] as well as green coffee, parchment, and roasted coffee when applicable.

Four Value Chain Types

For both countries, we identified four main types of value chains:

Coffee cooperatives or associations exporting internationally or selling to the domestic market

Intermediaries buying (usually parchment) directly from farms

Direct trade for export

Direct trade for the domestic market

Mapping Value Chains

The Impact of Direct Trade and Roasted Coffee Profitability in Colombia

Colombia is the world’s third-largest coffee producer, with approximately 550,000 coffee-growing families.[4] An estimated 25% of the rural population are coffee growers, with 96% classified as small-scale producers farming an average of 1.3 ha of coffee. Despite Colombia’s international reputation for quality coffee, only about 2% of farmers have been able to profit from the specialty coffee market.[5]

Families and Livelihoods

Of the eight families we extensively interviewed in Huila, seven produced specialty coffee and one produced commodity coffee. Most families produced dried parchment, although two produced and sold roasted coffee—these families had the highest livelihood outcomes overall. We learned that all the families earned some off-farm income, but the families who produced “specialty coffee” received higher prices and had longer-term relationships with buyers. Families that produced specialty coffee generally enjoyed higher social capital—including high credibility among buyers who were willing to pay price premiums.

Profitability by Processing Stage and Value Chain Type

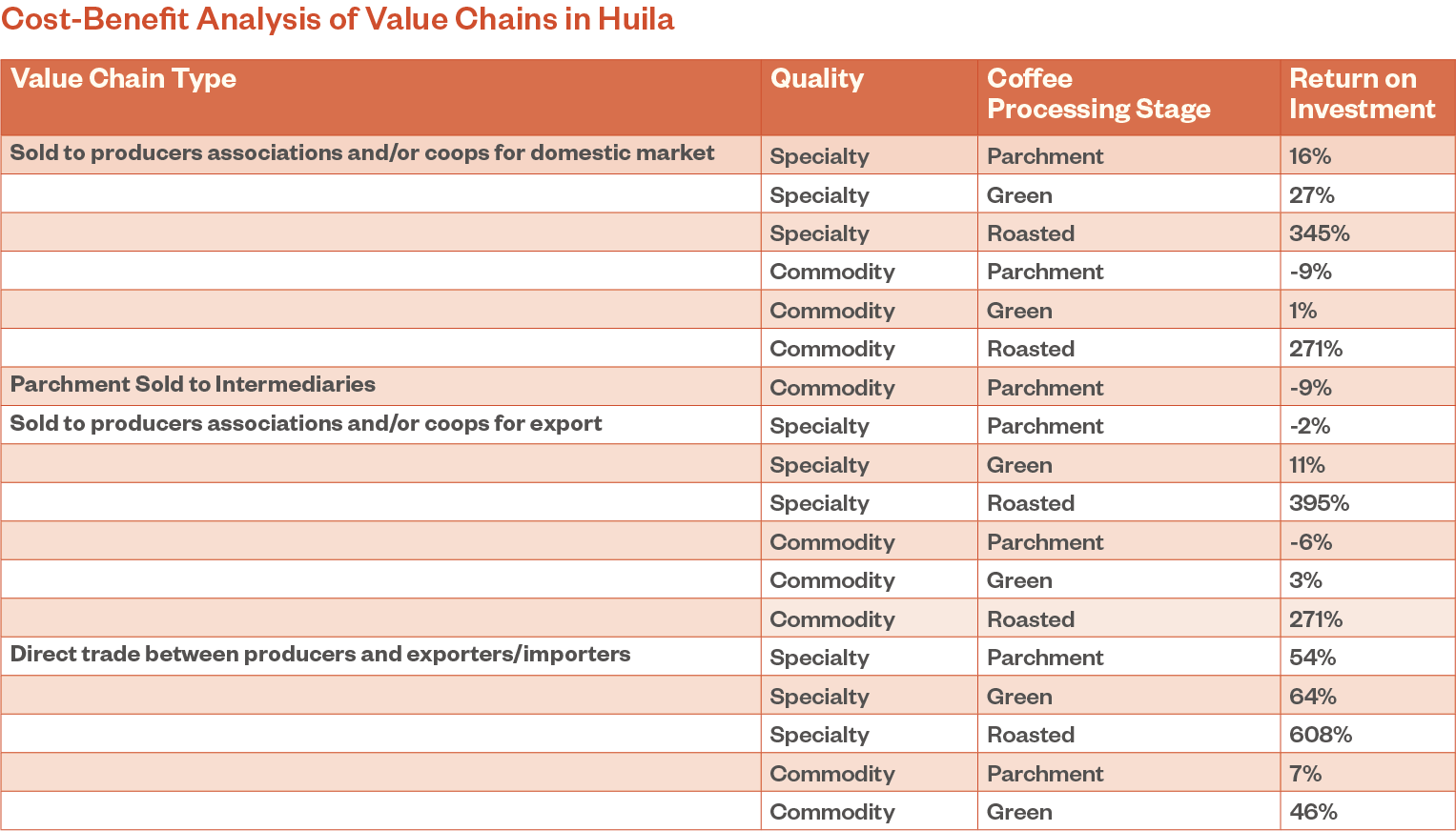

Our analysis of the value chain types found that the stage at which coffee was sold (parchment, green coffee, or roasted coffee) had a dramatic impact on profitability. We found that farmers sold commodity parchment at a loss in three out of four value chains which we studied, and specialty parchment at a loss in one value chain. Notably, for farmers selling commodity parchment directly to intermediaries, costs exceeded revenues by approximately 9% (see figure 2).[6] These farmers often relied on off-farm income, family labor, and accumulated debt to sustain their households.

Processing improved profitability, but returns depended heavily on the value chain. Specialty green coffee sold directly to export markets achieved 64% returns, while selling through cooperatives yielded only 11–27% for specialty and 1–3% for commodity coffee. Roasting showed the most dramatic increases. Roasted specialty coffee sold through direct trade yielded returns up to 608%, with roasted coffee achieving the highest returns across all value chains. Even commodity coffee became highly profitable when roasted (271% returns through cooperatives). As producers take on these downstream activities, value capture increases substantially, allowing coffee to shift from a primary agricultural product into the foundation of a more diversified and resilient livelihood strategy.

Across processing methods, direct trade between farmers and importers or exporters was consistently the most profitable. For example, while parchment and green coffee were barely profitable when sold through cooperatives or associations, they became substantially more profitable through direct trade relationships. In this context, it’s notable that the type of coffee product (parchment, green coffee, or roasted coffee) and value chain type had a larger impact on profitability than coffee quality (as determined by the 2004 SCA score). “The structure of coffee value chains—specifically who controls processing and who has direct market access—had a larger impact on farmer profitability than coffee quality alone, as measured by cupping scores.”

Figure 2. The results of the cost–benefit analysis for various forms of coffee sold through different value chains in Huila, Colombia, 2017–2020. The full calculations can be found in Jacobi et al., p.8.

The Pattern

Our research in Colombia revealed that the closer coffee production moves to consumption—through roasting and more relational value chains—the larger the share of value that remains with farmers, enabling them to improve their livelihoods. At one end of the spectrum, long value chains with limited processing, weak market relationships, and heavy reliance on intermediaries translated into low margins and heightened vulnerability for producers. At the other end were shorter, higher-value chains where farmers knew more about and were better connected to consumers. As producers took on more “downstream activities” (activities that bring coffee closer to the form in which it is consumed), value increased substantially, building the foundation for more diversified and resilient livelihoods.

Coffee-Cherry Products and Domestic Opportunities in Bolivia

Bolivia’s coffee—96% grown in the high altitude Yungas[7]—has high quality potential, but production remains small due to limited infrastructure, limited institutional support, and competition with other crops such as coca leaf.[8]

Coffee agroforests in the Yungas region, Bolivia.

Though traditionally favoring instant and torrado coffee,[9] Bolivia’s specialty consumer market is growing, with new roasters and cafés opening, including near production areas. The absence of an institution like Colombia’s National Federation of Coffee Growers means Bolivian farmers navigate price negotiations more independently. Families and Livelihoods One researcher spent one week each with four specialty coffee-producing families in the Yungas. All four families had very close relationships with their buyers and had comparatively higher livelihood outcomes than other coffee farming families in the region whom we interviewed.

Among other benefits, farming specialty coffee increased their income, improved their access to training, and allowed investment in infrastructure. However, three of the four families experienced a trade-off: their intensification of specialty coffee cultivation included a shift from traditional agroforestry systems to full-sun monocultures, leading to deforestation and greater use of synthetic fertilizers and pesticides. Many households also struggled with financial planning, credit access, and essential expenditures for health and education.

Profitability by Processing Stage and Value Chain Type

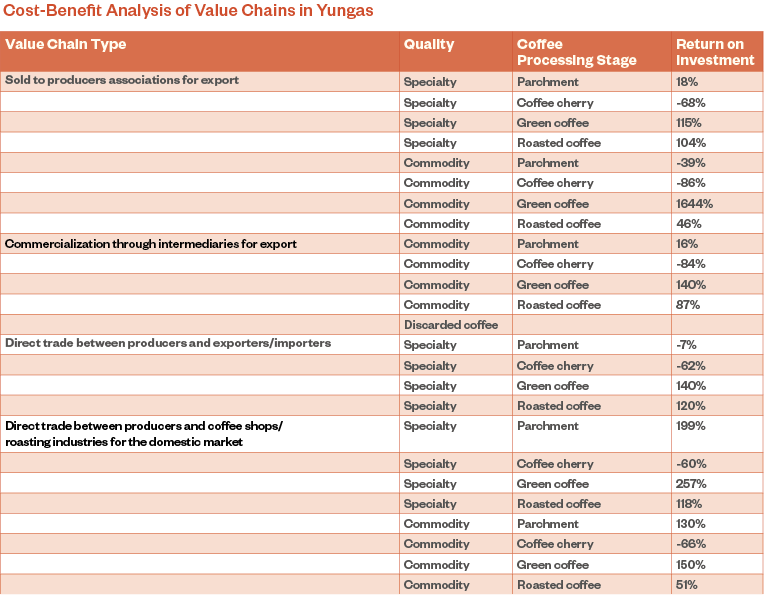

Our cost–benefit analysis revealed that Bolivia’s coffee value chains were characterized by narrow profit margins and high production costs. On a typical smallholder farm (1–3 hectares), production costs broke down into 53% labor (including family work), 30% external inputs, such as fertilizer and energy, and 17% basic services and administrative fees. Many value chain options resulted in losses or minimal returns.

Coffee-cherry products, despite their traditional use as sultana tea, consistently operated at a loss across all value chains, with negative returns ranging from −60% to −86% (see figure 3).[10] This reflected the low prices paid for this byproduct relative to processing costs.

Producers who brought their coffee to the green stage of processing improved their profitability for both domestic- and export-oriented value chains. The additional step of roasting coffee provided consistently high returns, though roasted specialty coffee yielded significantly higher margins than roasted commodity coffee. Unlike in Colombia, where roasting always provided the highest returns, in Bolivia the domestic direct trade of green coffee actually outperformed the domestic trade of roasted coffee.

Figure 3. The results of the cost–benefit analysis for various forms of coffee sold through different value chains in the Yungas, Bolivia, 2017–2020. The full calculations can be found in Jacobi et al., p. 8.

The Pattern

Selling coffee domestically was key to high returns in Bolivia: domestic trade delivered the highest or near-highest returns at every processing stage (parchment, green, and roasted). For specialty coffee, domestic direct trade yielded 199% returns for parchment, 257% for green coffee, and 118% for roasted coffee—substantially higher than export-oriented channels. This suggested that Bolivia’s growing domestic specialty coffee market offers particularly strong opportunities for farmers who can access it. The findings reveal that in Bolivia, as in Colombia, the value chain structure had a larger impact on profitability than coffee quality alone.

How Can Specialty Coffee Work for Farmers?

Our research in Colombia and Bolivia revealed that the structure of coffee value chains—specifically who controls processing and who has direct market access—had a larger impact alone—as measured by cupping scores. Across both contexts, we found that specialty coffee generated superior returns for farmers when they: (1) sold their coffee to associations that resold it to exporters with international clients, (2) sold directly to national and international clients, or (3) roasted the coffee and sold it directly. These three scenarios offered better returns than value chains with large numbers of intermediaries—especially when compared to selling parchment to intermediaries at the farm. Shorter value chains generally allowed farmers to increase their bargaining power and build long-term relationships with buyers.

Coffee-cherry soda, Caféteria Typica, La Paz 2019. Image credit: Azafrán Bolivia.

However, although our participatory research was able to identify these opportunities and build tangible projects, there are broader structural constraints that impact farmers. Families continued to struggle with access to quality healthcare, financial planning, and education, and transitioning to producing specialty coffee requires significant resources of time, training, and labor. Our research wasn’t able to address underlying dynamics of price pressure and market volatility, nor the power imbalances in value chains. Our research showed that independent small-scale farmers—and particularly women workers like the palliris (coffee sorters)—remained vulnerable and marginalized.

Positively, our consumer surveys and research found a growing tendency among specialty coffee shops in Bolivia and Colombia to work directly with producers, thus shortening the value chain and providing opportunities for high value retention for producers. Within these schemes we observed positive collaboration—including technical assistance in processing and training (in barista work, roasting, and cupping) for producers, as well as higher prices paid. In Bolivia specifically, selling to the growing domestic market was particularly advantageous, and we’re excited as these opportunities continue to grow.

The participatory research also led to lasting outcomes. In Colombia, a master’s course in “Coffee Science and Technology” now operates with Swiss partner support. In Bolivia, Universidad Mayor de San Andrés founded a “Coffee Excellence Centre” in collaboration with the University of Bern. Coffee-cherry products developed in the frame of the action research project with Slow Food and Azafrán, Bolivia 2019.

Coffee Cherry Flavour, a recipe book developed in collaboration with Slow Food Bolivia, chefs, and coffee farmers. The book is visible through https://digitalcollection.zhaw.ch. Coffee-cherry products developed in the frame of the action research project with Slow Food and Azafrán, Bolivia 2019.

In Bolivia, workshops with Slow Food Bolivia produced two handbooks on sultana (cascara) recipes and post-harvest practices, plus a campaign with tasting events and competitions with ANAPCAFE. These projects aim to increase profitability of cascara value chains by connecting traditional interests with innovators in the gastronomy sector. Beyond these specific outcomes, our researchers offered insights into how value chains impact the livelihoods of smallholder coffee farmers in two different contexts. In the more mature market of Colombia and the more emerging market of Bolivia, higher returns depended on a combination of quality, processing capabilities, training, and education, and—critically—the ability to participate in shorter, more relational value chains.

This co-authored feature is a summary of research conducted by CHAHAN YERETZIAN, NELSON GUTIÉRREZ GUZMÁN, and JOHANNA JACOBI, with contributions from researchers Derly Lara, Daniel Castro, Sebastian Opitz, Sabine De Castelberg, Sergio Urioste, and Alvaro Irazoque. Institutional partners included the Zurich University of Applied Science (ZHAW), The Universidad Surcolombiana, Slow Food Bolivia, and the University of Bern.

References

[1] You can read the full academic journal article at Johanna Jacobi, Derly Lara, Daniel Castro, Sebastian Opitz, Sabine de Castelberg, Sergio Urioste, et al., “Making Specialty Coffee and Coffee-Cherry Value Chains Work for Family Farmers’ Livelihoods: A Participatory Action Research Approach,” World Development Perspectives 33 (2024), doi.org/10.1016/j.wdp.2023.100551.

[2] As part of our research, we conducted an online survey of coffee consumers. In Colombia, 87% of respondents consumed coffee regularly, and in Bolivia 67%. In Bolivia, 114 respondents identified as “specialty coffee consumers” and 122 did not; in Switzerland, the numbers were 123 and 99 respectively; and in Colombia 207 and 100. It is worth noting, however, that despite Colombia’s international reputation for quality coffee, very few farmers—only about 2%—have been able to profit from the specialty coffee market to date.

[3] We also investigated a third research question that is beyond the scope of this article. “What value chain improvements, including policy reorientations, could help enhance the most beneficial types of specialty coffee and coffee-cherry value chains?”

[4] PMCA was developed at the CIP International Potato Center in Peru. Douglas Horton, André Devaus, Graham Thiele, Guy Hareau, Miguel Ordinola, Gaston López, et al., “Collective Action for Inclusive Value-Chain Innovation: Implementation and Results of the Participatory Market Chain Approach. Social Sciences Working Paper” (2020), Lima, Peru: International Potato Center, https://doi.org/10.4160/02568748cipwp20201.

[5] We defined “specialty coffee” as coffees that scored over 80 points in Colombia and over 83 points in Bolivia, according to the 2004 SCA scoring system. (We found that the 83 points was generally the threshold at which coffees began to receive price premiums in Bolivia.)

[6] We considered “commodity coffee” coffees that scored below 80 and 83 points in Colombia and Bolivia, respectively.

[7] FNC figures from 2022 in Jacobi et al., p. 2.

[8] Nelson Gutiérrez Guzmán, Derly Cibelly Lara Figueroa, Daniel Mauricio Castro Cabrera, Chahan Yeretzian, Sabine de Castelberg, Johanna Jacobi, and Sebastian Opitz, “Análisis de stakeholders y mapeos de cadenas de valor del café en Colombia” (2020).

[9] All percentages used in this section are drawn from table 4 in Jacobi et al., p. 8, adapted in figure 1.

[10] M. de Desarrollo, Rural y Tierras MDRyT, Sistema Integrado de Información Productiva, Ministerio de Desarrollo Rural y Tierras de Bolivia (2024).

[11] M. Rojas et al., Determinación del incremento del volumen de producción y la estructura de ingresos, costos a nivel de la finca familiar para los rubros productivos priorizado en la ENDIC y el PAPS II en el Trópico de Cochabamba y Yungas de La Paz, Fundación DECMA – NIRAS, La Paz (2017), p. 95.

[12] Walter Vásquez, “Seis de cada diez bolivianos consumen café con frecuencia,” El Financiero (2015).

[13] All percentages used in this section are drawn from table 3 in Jacobi et al., p. 7.

We hope you are as excited as we are about the release of 25, Issue 25. This issue of 25 is made possible with the contributions of specialty coffee businesses who support the activities of the Specialty Coffee Association through its underwriting and sponsorship programs.Learn more about our underwriters here.